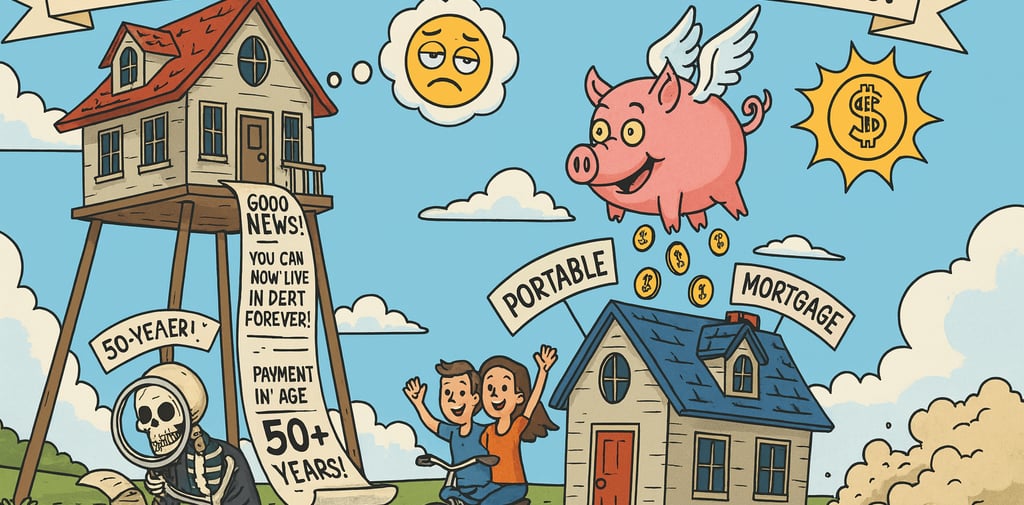

50-Year and Portable Mortgages: The Housing Market's Latest "Solutions" 🙄

Because apparently 30 years of debt just isn't enough anymore

Thomas Brady

11/16/20254 min read

Welcome to 2025, where homebuying has become so expensive that the financial industry is getting creative 💸. Rising prices? Check. Sky-high interest rates? Check. Long Island inventory tighter than a drum? Triple check.

Enter two shiny new ideas that policymakers and housing officials are floating around like trial balloons: the 50-year mortgage and the portable mortgage. Neither exists yet in any real, usable form, but boy, are people talking about them.

Let's break down what these "innovations" actually mean and whether they're brilliant solutions or just fancy ways to kick the can down the road (spoiler: probably the latter).

The 50-Year Mortgage: Because Who Needs to Own Their Home Before Retirement? 🏠⏳

For generations, the 30-year fixed mortgage was the gold standard. Solid. Reliable. A nice round three decades to pay off your slice of the American Dream. But apparently, that's not long enough anymore.

The pitch: Stretch your mortgage payments over 50 years instead of 30, which means lower monthly payments because you're spreading the principal out like butter over very, very stale bread.

Why Anyone's Even Talking About This 🤔

First-time buyers are priced out of the market (shocking, I know)

Politicians want an "affordability solution" that doesn't actually cost the government money

Renters might finally be able to buy... in theory

The "Benefits" (And I Use That Term Loosely) ✨

✅ Lower monthly payment than a 30-year mortgage

✅ Might help you technically qualify for a home you can't really afford

✅ Perfect if you're 25 and dream of making mortgage payments until you're 75

The Reality Check Nobody Wants to Hear ⚠️

❌ You'll pay a staggering amount more in interest over 50 years

❌ Equity builds at the speed of a glacier in January

❌ Buy in your 30s? Congrats, you'll be making payments into your golden years while your knees give out

❌ It's not even a "Qualified Mortgage" under current regulations (minor detail)

Long Island Translation 🗽

Here in Suffolk County, where a modest home costs more than a small yacht, monthly affordability is crushing buyers. Sure, a 50-year mortgage might get you through the door—but if you're planning to move within 10 years (and statistically, you probably are), you'll have built up approximately zero equity. Selling could actually hurt you financially. But hey, at least you'll have technically owned a home for a minute! 🎉

Portable Mortgages: Take Your Low Rate and Go 🧳🏡

This one's actually kind of clever, which is why it probably won't happen.

The concept: You lock in a great mortgage rate—say, 3%—and when you move, you get to take that rate with you to your next home.

How It Would (Theoretically) Work

Keep your existing interest rate, terms, and transfer it all to a new property

New house costs more? Finance the difference with a separate loan (at whatever terrible rate exists then)

Move freely without penalty

Why Policymakers Are Suddenly Interested 👔

Millions of Americans are sitting on mortgages with 2-4% rates and refuse to move because who wants to trade a 3% rate for a 7% one? This "rate lock" phenomenon is strangling housing inventory nationwide. If people could move and keep their rates, maybe—just maybe—more homes would hit the market.

The Upside 📈

✅ Move without losing your amazing rate (genuinely useful)

✅ Could actually help ease the inventory crisis

✅ Flexibility to relocate, upsize, or downsize without financial punishment

The Complications (There Are Always Complications) 🤯

❌ Lenders and investors need to figure out how to structure this without blowing up the financial system

❌ You'll likely still need additional financing for pricier homes

❌ Doesn't solve the fundamental problem: we don't have enough houses

Suffolk County Impact 🏖️

For Long Islanders trapped in homes they've outgrown (or that are too big now that the kids moved out), portable mortgages could be a game-changer. More movement = more inventory = slightly less insane competition. Slightly.

The Bottom Line: Choose Your Fighter 🥊

Both ideas are trying to address the affordability crisis, just in completely different—and potentially problematic—ways.

50-Year Mortgages 🐌

The Good: Lower payments, easier entry

The Bad: Crushing interest costs, equity that builds slower than your 401(k) during a recession

The Verdict: A mortgage that outlives your career and possibly your knees

Portable Mortgages 🎒

The Good: Keep your rate, increase mobility, help inventory

The Bad: Complex rollout, may still require expensive additional loans

The Verdict: Actually useful... which is why it'll probably take years to implement, if ever

What This Means for You 🤷

Look, neither of these options is coming to save you tomorrow. And honestly? They're Band-Aids on a bullet wound. The real problem is that we don't build enough housing, prices are astronomical, and rates are painful.

But if these tools eventually materialize, they could offer some relief—just understand the trade-offs. A 50-year mortgage might get you in the door, but you'll pay dearly for it. A portable mortgage might give you freedom, but only if the industry can figure out how to make it work.

Until then, the fundamentals remain: solid financial planning, expert local guidance (shameless plug 😉), and realistic expectations about Long Island's brutal inventory situation.

Welcome to the future of homebuying. It's creative. It's complicated. And it's definitely not your parents' mortgage market. 🏠💀

Thomas Brady, SFR, e-PRO, SRES, BPOR, C-REPS

Licensed Associate Real Estate Broker | Director of Operations

Notary Public | Retired N.Y.P.D. Lieutenant | U.S. Air Force Veteran

Vintage American Realty LLC

1551 Montauk Hwy., Suite E

Oakdale, NY 11769

📱 Cell: 631-682-8660

📧 Email: TomBradyHomes@gmail.com

🌐 Web: VintageAmericanRealty.com

Serving Suffolk County with straight talk and zero BS since... well, since before 50-year mortgages were a thing. 🎖️🏡

Vintage American Realty, LLC

Vintage American Realty, LLC is licensed in the State of New York

office: 631.319.4564

broker: 631.816.0719

info@vintageamericanrealty.com

1551 Montauk Hwy, Ste E

Oakdale, NY 11769

Long Island, NY